Markets in Motion: War, Inflation & A Global Reset

Middle East conflict shakes global nerves, US inflation shows signs of easing, and a renewed US-China trade deal brings back confidence (8-min read)

Last week was anything but quiet for global markets. On one hand, we saw a welcome slowdown in US inflation and a surprising breakthrough in US-China trade relations; both of which temporarily helped lift investor sentiment. On the other, escalating tensions between Iran and Israel introduced fresh geopolitical risk just as many major assets were testing all-time highs.

The clash in the Middle East sent a shock (pun slightly intended) through commodities and risk assets, reminding investors how quickly the market mood can shift. Meanwhile, the softer inflation data out of the US boosted hopes for future rate cuts, while the newly announced trade deal with China signalled a possible easing of economic friction between the world’s two powerhouses.

In this week’s breakdown, we unpack what these developments mean for the broader macro landscape - looking at their impact on oil and gold, equity markets, and of course, crypto. With rising uncertainty and shifting narratives, these recent events could also be a catalyst to add momentum to the strength of the US dollar.

Let’s get into it!

War Tensions Between Iran and Israel: Markets Brace for Impact

In one of the most dramatic escalations in recent times, Israel launched a wide-scale military operation against Iran just days ago, striking over 100 targets in a bold, pre-emptive move. The operation, called "Rising Lion”, aimed to dismantle key nuclear facilities and military infrastructure, including Iran’s heavily fortified sites at Natanz and Isfahan. High-ranking Iranian military figures were also targeted, sending a clear message: Israel is done waiting.

What was Israel waiting for?

Firstly, the International Atomic Energy Agency (IAEA) confirmed that Iran was delaying nuclear inspections, therefore heightening fears that a weapons-grade breakthrough was closer than many had assumed. Secondly, a two-month diplomatic deadline for Iran to re-engage in nuclear talks with the U.S. quietly expired. With patience wearing thin, Israel struck first and framed the attack as a ‘necessary step’ to prevent what it views as an imminent nuclear threat.

Considering Israel always seems to have an excuse to attack other countries first, I’d take their reasonings with a pinch of salt.

Iran wasted no time retaliating, firing waves of drones and missiles toward Israeli cities like Tel Aviv and Haifa. Israel claims it now holds air superiority over parts of Iran, but the situation remains tense and the world is watching. As expected, commodities were among the first to react. Gold, the traditional safe haven, spiked by around 1.5% as uncertainty gripped headlines; briefly brushing against new local highs as investors and traders sought to manage their positions. Oil prices also surged by over 7%, with Brent crude rising on the fear of potential supply disruptions in the Strait of Hormuz, a key transit route for global oil exports.

What makes this tension especially critical is its timing: global equities, particularly US tech stocks, are either at or flirting with all-time highs. This creates a vulnerable setup as any significant shock could trigger fast-paced corrections across overheated asset classes. With all that being said, market veterans will remember that this isn’t the first time conflict in the Middle East has threatened to boil over. History suggests that despite sharp escalations, geopolitical flare-ups between Iran and Israel often simmer down into ceasefires or temporary truces.

This could also be expressed by the surprising resilience shown in the S&P500 index and Bitcoin. Considering the various dramatic video footage on social media of the missile attacks, these assets remained quite resilient.

The S&P500 only dropped by around 1.1% and although Bitcoin saw a 3-5% dip, that’s quite a tame move for such a volatile asset.

Now, this does raise the concern of there potentially being more pain to come if these escalations continue, but while there’s always the risk of things spiralling, the probability of a full-blown war remains low (for now). Still, investors are hedging accordingly, and positioning is shifting defensively. If you're actively trading, this is a time to watch headlines and protect gains, especially in sectors sensitive to commodity price spikes.

US Inflation: Cooling, But Don’t Get Too Comfortable

The latest inflation report out of the US delivered a breath of relief to investors. Headline CPI rose by less than expected at 2.4% (expected was 2.5%), and core inflation, which strips out volatile food and energy, also continued its slow retreat from the previous 0.2% to now 0.1%. It’s the second month in a row inflation has printed cooler-than-expected numbers, signalling that the Fed’s tightening campaign may finally be gaining traction. As a result, equities cheered the news, with rate-sensitive sectors like tech and real estate posting strong gains on hopes that a Fed rate cut may be closer than feared.

It’s important to understand that although the year-on-year inflation figures came in lower than economists predicted, it still rose higher than the previous reading of 2.3%. So in total, US inflation has actually INCREASED by 0.1%. It feels like market participants are getting overly excited and not looking at the bigger picture. In my opinion, the Federal Reserve is unlikely to change their cautious stance just yet.

Aside from the potential threat of new inflationary pressures from the Iran-Israel conflict, another reason for my pessimism at these inflation numbers is that the numbers haven’t shown any material impact from the reimposed trade tariffs just yet.

Some experts caution that tariff-related inflation pressures often take months to seep through to consumers and producers. We’re only two inflation prints into the new trade dynamics, so while the data is promising, it’s still early to rule out delayed effects. That's why caution remains the dominant tone from the Federal Reserve, even as Wall Street grows increasingly eager for a rate cut.

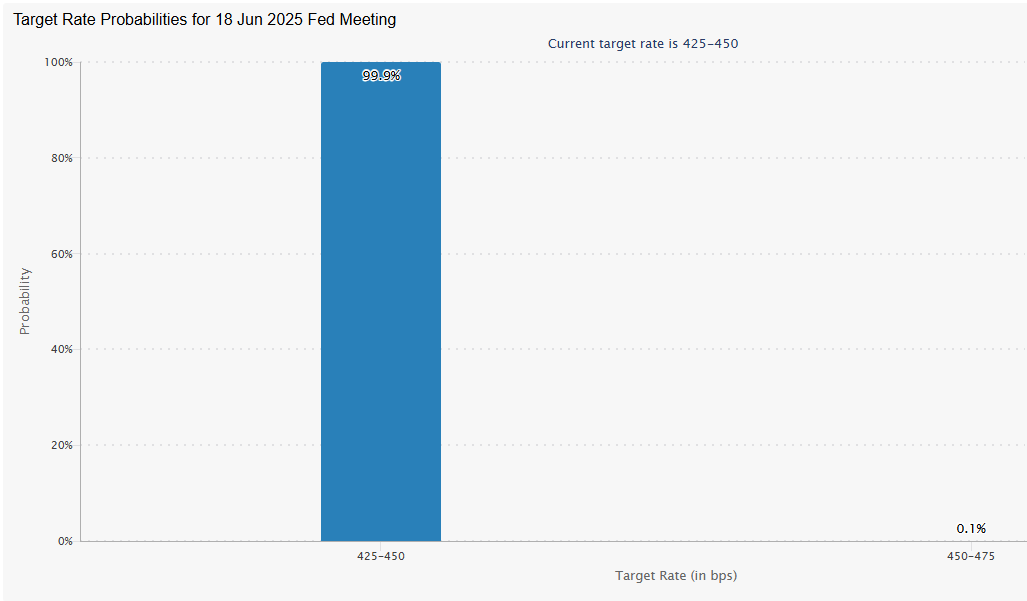

With the Fed’s next interest rate decision just around the corner (Wednesday 18th of June, to be exact), the market is currently pricing in a pause. Below we have a figure from the Fed Watch Tool (which is a real-time market-based gauge that shows how traders are pricing in the probability of future Federal Reserve interest rate decisions) and it shows a 99.9% probability of the Fed keeping rates the same. Of course this isn’t a crystal ball that knows exactly what the Fed will do at their meetings, but it’s a very useful piece of data to use in predictions.

Looking at the predictive data, a hold in rates is practically certain and amidst geopolitical uncertainty, it could actually strengthen the US dollar. If war tensions escalate and investors rush to safety, the dollar may bounce sharply -particularly since it's been hovering near a three-year low. From a trading perspective, this sets up a compelling risk-reward thesis: buying strong assets at their weakest point, especially if macro catalysts line up, can generate large returns. A pause from the Fed plus global uncertainty might just be the spark the dollar bulls have been waiting for.

US-China Trade Deal: A Surprising Turn Toward Stability

Lastly, In a move that caught many analysts off guard, the US and China have agreed on a fresh trade framework aimed at easing tensions and boosting economic cooperation. The deal focuses on reducing certain non-critical tariffs, improving access for US businesses in China, and outlining a clearer path for bilateral investment. While it doesn’t fully roll back the trade war measures of previous years, it’s a meaningful step in the relationship between the world’s two largest economies.

This deal couldn’t have come at a better time. As the global economy faces pressure from geopolitical tensions and slowing growth in some regions, a trade breakthrough injects a much-needed dose of stability. For the US, this deal is more than just economic, it’s symbolic. It signals to global investors that America still holds strong diplomatic and economic leverage, and that it's capable of negotiating constructive outcomes.

In short, Trump may say a lot of sh*t, but he wants to show the world that he can still achieve concrete results.

For the dollar, this deal adds another tailwind (for those not familiar with the term, “Tailwind” means a supportive factor or condition that helps drive growth).

With confidence returning to the US political and economic stage, foreign capital is likely to continue flowing into dollar-denominated assets. Combined with the Fed’s cautious stance and the global appetite for safety, the renewed trade cooperation strengthens the narrative for a sustained dollar rebound. Whether you're holding US equities, trading forex, or just watching from the sidelines, these recent events could be shaping a new chapter in global market sentiment as we enter the summer.

Key Takeaways For You This Week

Israel launched a large-scale pre-emptive strike on Iran targeting nuclear and military sites after stalled inspections and diplomatic talks, sparking market volatility. Gold and oil surged, equities held firm, but risks of further escalation remain.

US inflation came in slightly cooler than expected, boosting equities and rate-cut hopes. But with year-on-year CPI still rising and tariff effects yet to kick in, the Fed is likely to stay cautious, especially as war tensions and a potential dollar rebound add to the complex macro backdrop.

I hope you’ve learned something new, and if you have any questions or want anything to be clarified, please leave a comment below and make sure to follow us on all social media pages.

Instagram: @lets.speculate / TikTok: @lets.speculate / X: @_LetsSpeculate